){kind=link}

By Guoxiong Zhang, Ph.D., Shanghai Director of the Economist Intelligence Corporate Network (EICN)

‘China’s Economy: Key Trends in 2022’ was published in the fall 2022 edition of the German Chamber Ticker. Editor: Noga Feige, Senior Editor of Ticker Magazine. Visuals: Matter Design.

China’s real GDP grew by 8.1% in 2021 relative to 2020, which is remarkable given the size of the Chinese economy and China’s 2.3% growth rate in 2020. That being said, the journey of the Chinese economy in 2021 has been anything but smooth. Starting from the third quarter, growth expectations have been falling while concerns over high inflation have been rising. With the whole country being mobilized for its dual targets of peaking carbon emission by 2030 and reaching carbon neutrality in 2060, risks associated with China’s de-carbonization process have also emerged. Anti-trust and data regulations have been tightened, which increases the costs of innovation for the Chinese tech companies and narrows the space for them to make profits. While RCEP comes into force in 2022, ratification of the investment deal between China and the EU (CAI) has been put on hold. Evergrande’s default crisis, although not likely to trigger a global or national financial crisis, has spurred concerns over the high leverage ratio and liquidity issues of China’s real estate companies, casting a shadow over the outlook of China’s real estate industry. Looking ahead, how will the Chinese economy evolve in 2022? In my view, there are six key trends that we need to watch closely.

-

Growth and Inflation

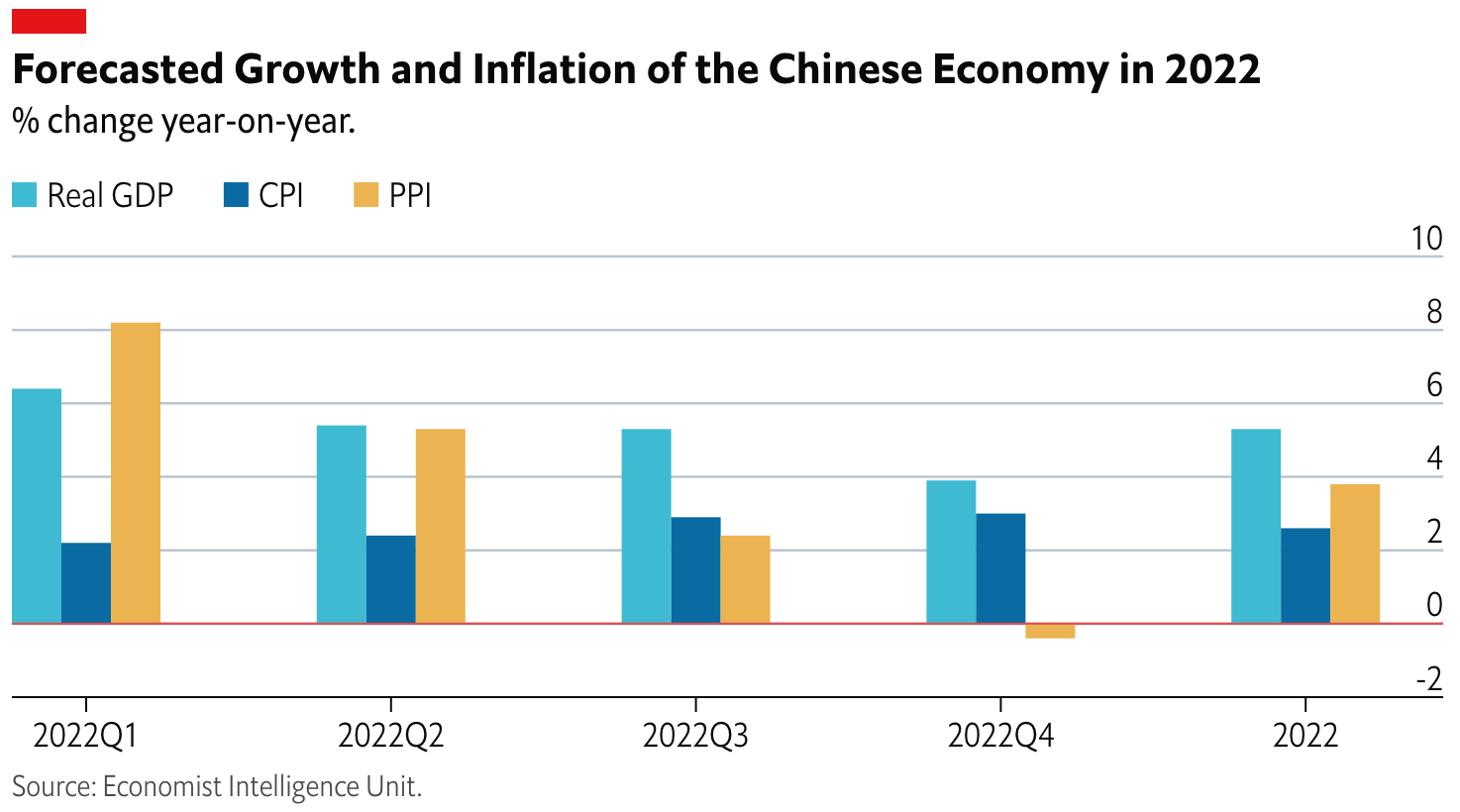

China’s real GDP growth in 2021 has been in a downward trend, even accounting for the base effect in 2020. The growth rate fell from 18.41% in the first quarter to 4.94% in the third quarter and slid further to 4% in the fourth quarter. In December 2021, the annual Central Economic Work Conference acknowledged the challenges from both the demand and the supply sides to the Chinese economy, and placed economic stability as the top priority for 2022. In the context of the Chinese economy, stability usually refers to a stable growth rate, which in my view is likely to be 5% or higher in 2022. According to EIU’s forecast, China’s year-on-year real GDP growth rate will have a downward trend in 2022, starting at 6.6% in the first quarter and reaching 3.5% in the last quarter. Over the whole year, the Chinese economy will grow by 5.2%.

As China’s producer price inflation exceeded 10% in the last quarter of 2021, there has been a wide discussion about the possibility of China entering stagnation in 2022. In my view, the chance is very small. First of all, an economy cannot stagnate if its growth rate exceeds 5%. Secondly, the Chinese economy is not likely to face high inflation in 2022. Commodity prices will be stabilized in 2022, and so will the producer price. According to EIU forecasts, the Producer Price Index (PPI) will fall from 8.2% in the first quarter to below zero in the fourth quarter. The Consumer Price Index (CPI) will fluctuate between 2% to 3%, which is still low by global standards.

-

Accommodative Fiscal and Monetary Policies

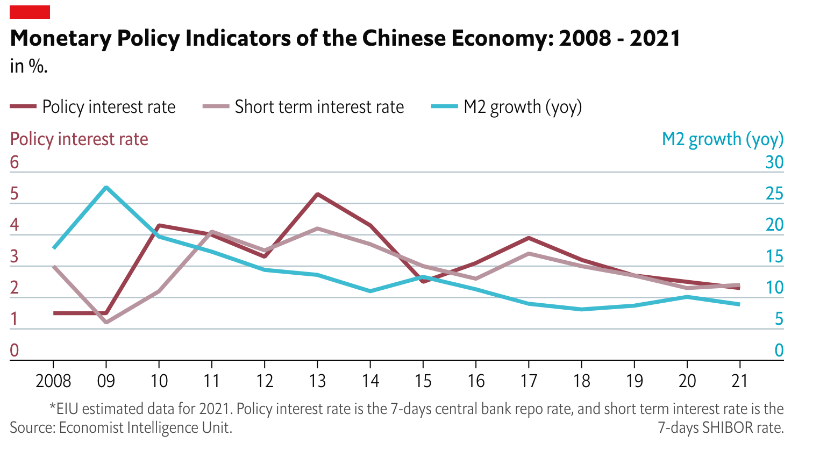

With the annual Central Economic Work Conference explicitly demanding more supportive policies for economic stability in 2022, both China’s fiscal policy and monetary policy are likely to be more accommodative this year. China does have the capacity to do so. Unlike other major economies, China did not have large-scale fiscal or monetary stimulus during the pandemic. In 2021, based on EIU estimates, both China’s budget deficit and public debt growth have been normalized to their pre-pandemic levels. Despite several rounds of deposit reserve ratio cuts, China’s monetary policy, in general, has been prudent last year. Its policy rate was slightly lower in 2021, but its short-term interest was actually higher in 2021, and its M2 growth slowed down in 2021 as well.

Regarding its fiscal policy, China will increase its public spending, but is not likely to initiate another RMB four trillion stimulus package. Projects related to people’s livelihood, new infrastructure, and China’s de-carbonization initiatives are more likely to receive increased public funding or investment. For monetary easing, the People’s Bank of China (PBoC) will be cautious, as the US is likely to start exiting quantitative easing in 2022, and China’s monetary policy has often been avoiding large RMB exchange rate fluctuations. In addition to further cutting required deposit ratios and injecting more liquidity through open market operations, the PBoC will also rely on window guidance to channel more liquidity into SMEs and projects mentioned above.

-

De-carbonization Initiatives and the Associated Risks

China has pledged to peak carbon emission by 2030 and to reach carbon neutrality by 2060. As EIU forecasts China’s CO2 emission to peak at 9,321 Mt in 2028, it will not be a challenge for China to achieve the first goal. The second goal is more challenging, and therefore China will need to use the rest of this decade to develop the right standards, markets, and technology. Risks similar to the regional power shortage that happened in 2021 will keep emerging in this learning-by-doing process. The recent Central Economic Work Conference called for more cautiousness in designing de-carbonization policies. It emphasized the importance of setting realistic targets, which echoes the Guideline for Achieving Carbon Neutrality that was published earlier by China’s top policymakers. In the Guideline, risk control is listed as one of the five guiding principles. In 2022, more specific regulations on de-carbonization will be established, and the existing carbon emission rights trading markets will also be expanded.

-

Regulation and Innovation

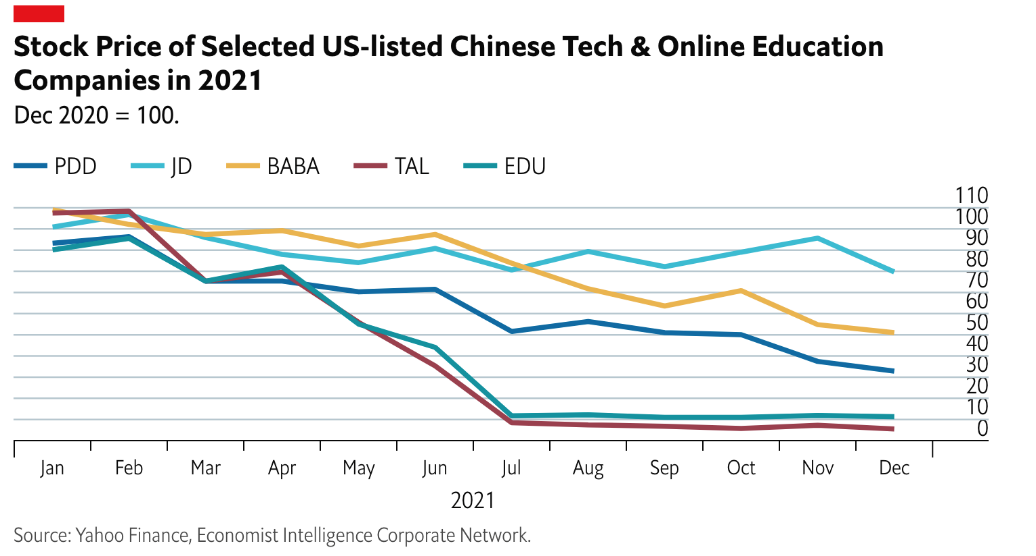

In China’s 14th five-year-plan, there is a clear message of shifting away from growth-centric development strategy to social development. One outcome of this changing priority is China’s strengthening enforcement of its anti-trust law and tightening its regulation on data collecting and usage, which affect Chinese technology companies the most. In the short run, more stringent regulations will hinder these technology companies’ innovation, and may cause them to lose their competitive edge over their US counterparts. Such regulations are not likely to be eased in 2022, as they were re-emphasized in the recent Central Economic Work Conference, which also demanded restricting private capital from accessing certain sectors. Nevertheless, as economic stability is placed on the very top of China’s economic agenda in 2022, such regulations are expected to be more specific and more formalized, which will reduce the uncertainty and shorten the time for the technology companies to adjust accordingly.

-

RCEP, CAI, and CPTPP

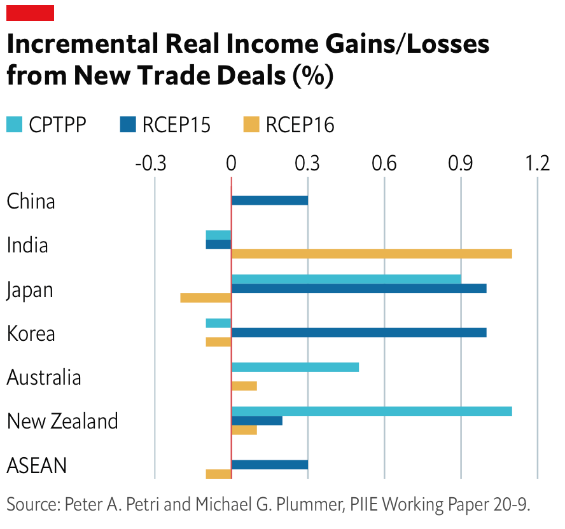

China’s determination to economically integrate itself with the rest of the world is evident from its decision to join RCEP. This trade deal, which came into force on January 1, 2022, will bring limited economic gains to China, while Japan and South Korea will benefit the most from it. In the investment deal with the EU (CAI), China has made huge amounts of commitment to EU investments, while the EU’s commitment to China is not clear and very likely to be limited. China has also applied to join CPTPP and declared its willingness to undergo domestic reforms to comply with CPTPP rule. Ratification of CAI was put on hold by the EU in 2021, and the chance of resuming it in 2022 is not clear at this stage. For China joining CPTPP, it is not likely to be materialized in 2022. How RCEP plays out in 2022 will affect the progress of CAI and China’s admission to CPTPP.

-

Outlook of China’s Real Estate Sector

The default crisis of Evergrande, one of China’s largest and most leveraged real estate conglomerates, has not spurred much worry among people in China about a potential national, or even global, financial crisis. But it did cast a shadow on the outlook of China’s real estate sector, which has already been gloomy after China’s deleveraging campaign in 2016 and its attempt to curb housing speculations in recent years. But in the foreseeable future, the real estate sector will remain important to the Chinese economy. In 2020, real estate and construction combined contributed more than 15% of China’s GDP, and real estate investment took more than 20% of China’s fixed capital investment. With an urbanization rate of 60% in 2020, China’s urbanization will continue, albeit at a slower pace. Given the large spill-over effect of the real estate sector, policymakers will need to stabilize the real state sector for the sake of economic stability in 2022. More importantly, over 800 million people are already living in the city, and they need residential and commercial real estate services.

The real estate sector should grow along with China’s economic growth and urbanization process. Despite the risks brought by the real estate developers’ leverage appetite, China’s real estate sector by itself is as good as other sectors that have been contributing to China’s economic growth and modernization. 2022 will be a year of stabilization for China’s real estate sector, which is not favored by the policymakers, but is not dispensable to the Chinese economy.

Guoxiong Zhang, Ph.D., is the Shanghai Director of Economist Intelligence Corporate Network (EICN). Dr. Zhang creates and delivers the EICN programs and services in Shanghai. He is also leading EICN’s economic and business research in China. In his current role, Dr. Zhang has been advising senior executives from EICN’s member companies with macroeconomic and strategic insights.

Before joining The Economist Group, Dr. Zhang was an Assistant Professor of Economics at Antai College of Economics and Management, Shanghai Jiao Tong University. He was also a Visiting Scholar at Kellogg School of Management, Northwestern University.

Dr. Zhang has extensive research experience in the Chinese economy, particularly China’s monetary and fiscal policies, from both academic and policy perspectives. His research on the Chinese economy started at the Asian Development Bank in 2011, where he studied the macroeconomic consequences of Renminbi appreciation. As a faculty member at Shanghai Jiao Tong University, Dr. Zhang leads two state-funded research projects as the principal investigator.

Dr. Guoxiong Zhang graduated from the University of California, Irvine, with a Ph.D. in Economics and an MS in Statistics. He also holds a BA in Economics from Zhejiang University.